Reading the pulse

December 1, 2024

4 mins

.jpg)

The coalition government and markets will stabilize soon, and we will quickly transition to the next macro event within the strong structural bull market.

Yet, as traders, we often find ourselves in a strange metaphorical BDSM relationship with our bureaucracy and FM. Most black or white swans have turned into complex shades of gray.

So, how can we prepare for it?

Likely that Indians today feel more pride in their country than they have in the past 78 years. I reflect on several marvellous accomplishments including the implementation of UPI, Covid vaccinations, infrastructure development, internet affordability, Article 370, and India's growth story, among others.

However from a trader's perspective, I find the last ten years of the Modi sarkar to be a perplexing mix of Dr. Jekyll and Mr. Hyde. The "Ache din" have been exceptional, but we often find ourselves grappling with bizarre policies that seem to stem from a distorted understanding of socialism, and a futile effort to protect the not-so gullible retailers from themselves.

When the SEBI Chairman labels a market as a bubble or frothy, it essentially passes judgment on its own investors. At least in their view they are irrational, greedy, and possibly even foolish to invest or stay invested. By doing this, it removes any possibility of understanding why investors in that market are pricing assets as they do, which is crucial for formulating better regulations.

On the other hand, in the doglapan pro-max scenario, exchanges now offer option expiries almost every trading day, causing retail derivative volumes to skyrocket. Combine this with attempts to curtail mutual fund inflows, suffocating ASM/GSM measures, reduced F&O margins, and a plethora of taxes. This concentrates liquidity in fewer stocks, depleting the broad-based, stable liquidity that is crucial for a growing economy's capital market. Ironically, this ends up harming the same retail traders that the regulators aim to protect.

Many peer U.S. traders and prop desks, enticed by India's growth story, have tried but withdrew from trading in the Indian markets due to its poor market depth. Despite being the fifth-largest economy in the world, the average participant in the stock market is often treated like a peasant from the medieval feudal system.

Most traders and investors mistakenly believe that trading costs become smaller as portfolios become larger. While this is true for brokerage fee, which might be the only cost they pay explicitly, there are three other costs (from the lectures of Prof. Damodaran) that are incurred in the course of trading that are much higher than the brokerage costs

For us, as momentum traders, the bid-ask spread essentially represents the difference between the price at which we intended to buy the stock and the actual price at which the buy order was filled. This difference is often the buffer between the trigger price and the limit price.Since the trigger price is typically higher than the current price, awaiting a breakout, there's always a risk of partially filled orders or no fills at all. The risk significantly increases when you trade with tight stop losses (1-4%) and seek to execute a larger position within a narrow price range.

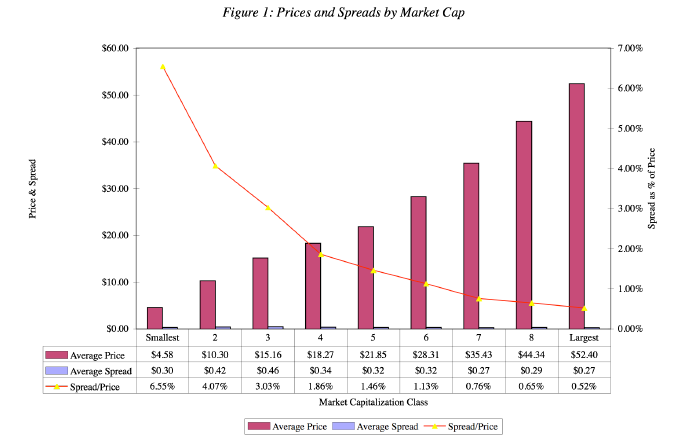

A study by Thomas Loeb in 1983, compared the bid-ask spreads of stocks in NYSE with respect to their average price and market cap, as summarised below -

Although the dollar spread does not significantly differ across market caps, stocks of smaller companies tend to be lower priced. As a result, the spreads were as high as 6.55% of the price for small cap stocks, and as low as 0.52% of the price for large cap companies. This could explain why renowned momentum traders such as O'Neil, Ryan, and Minervini implemented wider stop losses (7-10%), a practice that continues to be blindly followed without considering the current context.

One could argue that these studies are outdated, given the significant changes in both market structure and spreads in the financial markets. However, in the Indian context, where ~70% of the free-float market cap of NSE stocks is concentrated in the top 100 stocks, the spreads in the remaining 2000+ companies are noticeably poor. Therefore, the cost of a wide bid-ask spread for trading these companies must be taken into account.

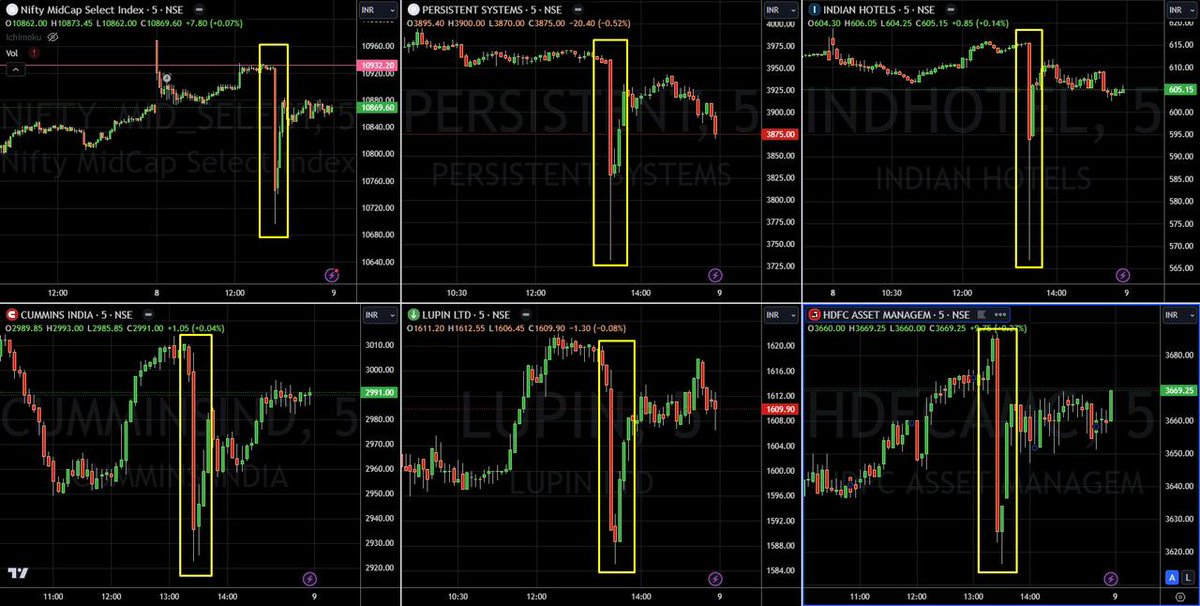

In an illiquid market, a large trade creates an imbalance between the buy and sell orders, and the only way it can be resolved is with a price change. While this change is temporary and will reverse when liquidity returns to the market, it results in erratic spikes and shakeouts, making execution difficult for traders with stop losses. Trading consistency problems often stem from not accounting for these price impact costs in illiquid counters. It has particularly affected option participants, where the passive house edge of the sellers and expiry players has considerably diminished. This has led to 'ant-sized' gains shrinking further and the probability of 'elephant-sized' losses increasing.

This is an example of how a tandem liquidity grab, also lovingly referred to as "injections" by @jitendrajain, could potentially jeopardize your entire house edge.

8th April 2024 MidCap expiry -

Even in the cash segment, a large chunk of volumes often get concentrated on block deals and private offline transfers to avoid the price impact of large trades. For instance, Elantas Beck India, a company listed on the BSE, currently has a market cap ~Rs 9400 crore. It's one of the top holding of the Nippon Small Cap Fund (the largest small cap fund in India), with a stake worth ~Rs 700 crore.

The stock price has seen over 200% growth in the past 18 months.However, the stock is absolutely illiquid and untradeable. Here's what the intraday chart looks like

This is not supposed to be an adverse observation about the company or mutual fund, but the liquidation of a 700 crore holding, when the average turnover on BSE is less than 2 crore, would likely occur through private placements and off-market block deals.

These illiquid markets and stock counters become more vulnerable to artificial manipulation, turning into a playground for liquidity grabs and concentrating profits within a select few entities, like Jane Street. The fundamental principle of capital markets, which is to be fair and a method for efficient price discovery, gets absolutely destroyed.

A trader or investor can minimize the bid-ask spread and price impact costs by splitting large blocks into smaller ones and trading over a longer period. However, there is a cost associated with waiting. You often end up buying at a much higher price, especially if you are a breakout trader, which reduces the expected profits from the trade. Additionally, the price may rise so much that the trade is no longer worthwhile.

These are some of the execution changes that have been implemented as the portfolio has scaled up over the past few years -

Even though I generally use tight stop losses (1%-3%), I still add a 0.3%-0.6% buffer to provide for slippages over a sample set of trades. Despite all the applied liquidity filters, when the breakout squats, it's common for the volumes or bid-ask spreads to be thin, leading to slippages. Even a small 2% price slippage is nearly double the risk initially taken. This is why trade journal analysis and post reviews are critical—tracking slippage patterns helps you refine your buffers and execution.

I usually do not wait for the stop loss to be triggered. Since technical reasons often drive my buying decisions, any sign of weakness, such as breaching the lows of the breakout bar, prompts me to consider staggered liquidations. This procedural memory and execution skill has greatly benefited me. I have been able to consistently reduce my average loss to less than 1.5%. Implementing tight stop losses with aggressive position management also amplifies the impact of bigger winners on a portfolio.

Once your portfolio exceeds a certain size (1cr+), focusing exclusively on velocity or swing trades with tight stop-losses for rapid profit turnover isn't viable anymore. The focus shifts towards positional strategies with longer holding periods and higher risk and position sizes in liquid stocks.

Some stocks meet basic liquidity criteria based on turnover scans but have wide bid-ask spreads and lack transaction depth. Stocks with multiple blank or low-volume bars on the intraday charts (3/5 min) are typically avoided (like Elantas).

All stocks in the 5% circuit are avoided.

Priority is given to setups like IPOs or Episodic Pivots (read here - https://bit.ly/EpisodicPivots). These setups naturally attract liquidity, are more scalable, and offer multiple entry points for smooth position building and exit.

Even reversal setups provide good liquidity, but they offer limited risk-reward opportunities and occur infrequently, so I seldom trade them.While the risk of transaction costs is subjective and depends on the individual, it's better to err on the side of caution. This approach optimizes your execution for scalability.

I never use market orders for executing trades. While an unfilled or partially filled order can be managed and optimised by maintaining sufficient buffer between the trigger and limit price, slippages in an illiquid stock can disrupt the whole trade, especially when leverage is involved.

In any trading setup, there are always clear order clusters near trendlines, swing highs, or resistances. This is where new technical traders or CMT bravado's often place their orders. It's necessary to identify these “obvious” zones and execute your orders before the price reaches them. Situational awareness in trading helps you identify these crowded zones and find better execution points away from obvious order clusters. Situational awareness in trading helps you identify these crowded zones and find better execution points away from obvious order clusters. This way, the orders that trigger after your entry can provide a cushion for your entry. This allows you to raise your stop-loss orders and reduce risk more quickly. (read more about this here - https://bit.ly/PositionSizingMgmt)

It's crucial to maintain flexibility in the placement of entry and stop-loss orders, adjusting them according to the live stock movements and volume clusters observed in the market depth. For instance, entries around previous day highs (PDH), swing highs, and opening range highs (ORBs) are becoming crowded due to their growing mentions on social media. However, it's beneficial if such trends continue to revolve, as they provide savvy traders with new and recurring edges in execution.

If my trailing stop loss is far from the current market price, I don't set the stop loss in the system. Instead, I set alerts 2-4% away. This strategy helps avoid being shaken out by erratic moves and losing out on unrealised profits.

India disappoints both optimists and pessimists (by Ruchir Sharma). But I believe it will disappoint a lot more pessimists than the optimists in the next 20 years.For individual traders, the risk in the next ten years is more with missing out on the upside potential rather than evading the downside. This necessitates mastering the art of scaling up your portfolio amidst a spectrum of liquidity risks.

December 1, 2024

4 mins

September 1, 2023

7 mins