Reading the pulse

June 16, 2024

8 mins

.jpg)

The Indian markets had been too good for too long.Such bull markets often hide systemic flaws—particularly the dangerous habit of remaining completely on the sidelines during corrections and passively waiting for easier conditions to return.

Merely preserving capital in such periods isn't sufficient risk management. Here's why:

For momentum traders, avoiding a prolonged and deep market correction is straightforward—it simply requires the basic practice of setting a stoploss and adhering to it. During such corrections, purists often recommend staying in cash and waiting for favourable conditions, with the thesis that mastering a single setup during bull runs is sufficient for trading success. While it's a safe and noble stance to take, they're more wrong than right in the Indian context.

In theory, there is no difference between theory and practice. In practice, there is.

Here, market liquidity is shallow, the stock universe is relatively small, and SEBI swiftly places fast-moving stocks under its ASM framework. The risk of under trading is just as significant as, if not more than, the risk of getting chopped around by overtrading.

The portfolio return equation for any stock market player can be broken down into a simple formula: Expectancy × Frequency, where

Expectancy = (Average Winner % × Win Rate) - (Average Loss % × (1 - Win Rate)) = How much larger your winners are compared to your losers

Frequency = Number of trades taken

Within this equation, swing trading often ends up becoming a half-assed, confused technique. It lacks both the agility of day trading and resilience of positional trading.

The typical cycle for a swing trader unfolds like this: You shift to full cash during a correction, then spend 5–15 days gradually redeploying your capital as stocks begin to set up. After a few days of upswing, another correction or pullback triggers stop losses, forcing a return to cash—and "The Cycle" repeats.

Moreover, selling positions in strength while using progressive exposure restricts effective capital utilization—typically averaging ~50% annually—which restricts maximizing both expectancy and frequency. As a result, swing traders end up spending a large portion of bull markets only cycling in and out of positions—neither building large enough positions to capture magnitude moves, nor executing enough trades to effectively churn capital for super performance. This is where setup prioritization transforms your approach.

While this approach may work in U.S. markets with no circuit filters and more opportunities and liquidity, blindly applying these strategies to Indian markets is like trying to chase a 50 over target in just 20 overs.

Often in "The Cycle," one or more key parameters (expectancy, frequency, or capital utilization) becomes severely compromised with pure swing trading, making super performance statistically impossible. Thus many successful traders in India have ended up leaning towards one style more—they are either more day traders or more positional traders, than swing traders. Trying to find an equilibrium between both across different market cycles is a tricky, high-effort, low-reward game.

There are two possible causes for inadequate returns— A) targeting a high return but getting thwarted by negative events B) targeting a low return and achieving it.

The moment we decide to become a trader or active investor, we've already chosen option A—pursuing exceptional returns with manageable risks—rather than option B, the more conservative path of long-term SIP investing. Therefore, underperformance should only occur when we've taken appropriate risks but failed to generate asymmetrical returns—indicating a skill gap that needs improvement. Underperformance should never result from failing to take enough calculated risks.

Going completely in cash at every market pullback, without expanding your skillset to new setups or exploring alternative asset classes and timeframes—isn't risk management; it's risk avoidance, which leads to return avoidance too. This is especially criminal if you're starting out with small capital, where aggressive capital compounding is crucial for making your efforts worthwhile. It requires being indifferent to small profits that don't materially change your life.

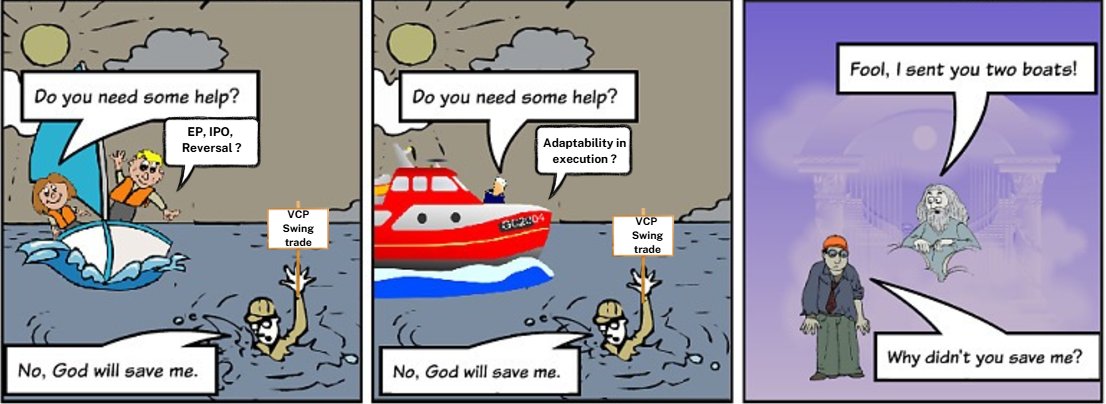

I believe our primary challenge isn't a lack of exposure to the science of market principles, and trading setups built around them. Rather, it's our reluctance to venture beyond familiar patterns and adapt our execution based on each setup's objective, strength, and context.

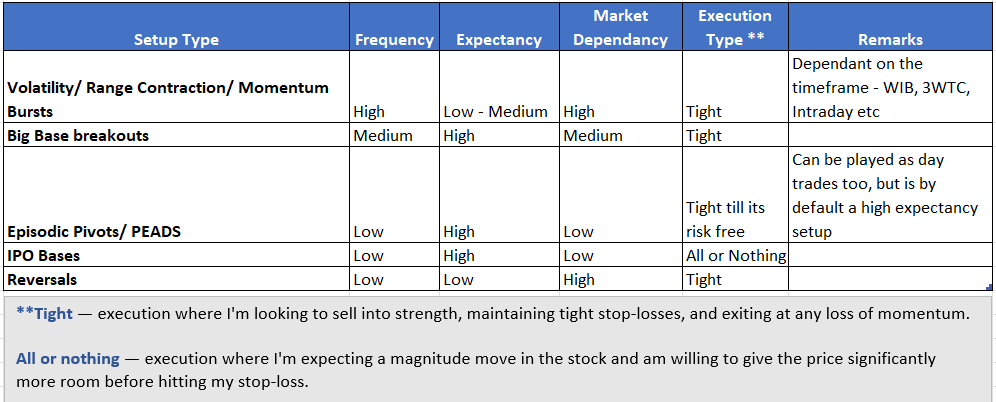

Here are the common setups used by momentum traders:

There are two common mistakes that I made and have been correcting, and that I see many others continue to make:

1) Managing high-expectancy setups like IPOs and EPs too tightly as if they were frequency trades, resulting in shakeouts

2) Taking an all-or-nothing approach with high-frequency, lower-expectancy trades like momentum bursts, despite knowing that breakout success depends heavily on market sentiment—resulting in squats

Using the same execution style across all setups, is where a lot of underperformance and frustration occurs, as it under-utilizes both expectancy and frequency. Creating a setups playbook helps standardize your approach across different setup types. There is always a favourable time for some or the other setup in the market, either in a different asset class (equity, commodities, currency, crypto) or on different timeframes.

A fantastic example of this was how Minervini adapted his execution methods in the USIC 2021. He noticed the lack of follow-through in breakouts and adjusted his strategy to focus on short-term trades lasting 1–5 days and scalps. He ended up winning the USIC with 334.8% in a difficult year (the runner-up was far behind at 100.4%).Even for the wizard, the setup is only as good as its execution.

The truth is, regardless of your experience level, you can never predict with certainty which trades will succeed or how far they'll run. In any given set of trades, some will win and some will lose, and the magnitude of the winners often catches us by surprise. The key isn't knowing the outcome—it's positioning yourself for opportunity as many times as possible. And in the Indian markets, we don't have the leeway to miss many of these opportunities.

Trade the market you are in, and not the market you wish you were in.

June 16, 2024

8 mins